BALANCED, SURPLUS AND DEFICIT BUDGET

1. The government may spend an amount equal to the revenue it collects. This is known as a balanced budget. If it needs to incur higher expenditure, it will have to raise the amount through taxes in order to keep the budget balanced.

2. When tax collection exceeds the required expenditure, the budget is said to be in surplus.

3. However, the most common feature is the situation when expenditure exceeds revenue. This is when the government runs a budget deficit.

Measures of Government Deficit

When a government spends more than it collects by way of revenue, it incurs a budget deficit. There are various measures that capture the government deficit and they have their own implications for the economy.

Revenue Deficit

The revenue deficit refers to the excess of government’s revenue expenditure over revenue receipts.

| Revenue deficit = Revenue expenditure – Revenue receipts |

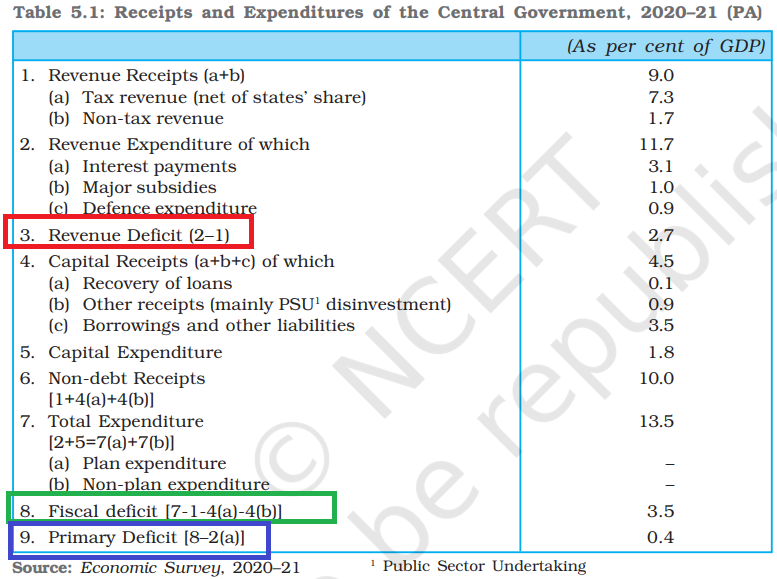

1. Item 3 in Table 5.1 (RED BOXED) shows that revenue deficit in 2020–21 was 2.7 percent of GDP.

2. The revenue deficit includes only such transactions that affect the current income and expenditure of the government.

3. When the government incurs a revenue deficit, it implies that the government is dissaving and is using up the savings of the other sectors of the economy to finance a part of its consumption expenditure. This situation means that the government will have to borrow not only to finance its investment but also its consumption requirements.

4. This will lead to a build up of stock of debt and interest liabilities and force the government, eventually, to cut expenditure. Since a major part of revenue expenditure is committed expenditure, it cannot be reduced. Often the government reduces productive capital expenditure or welfare expenditure. This would mean lower growth and adverse welfare implications.

Fiscal Deficit

Fiscal deficit is the difference between the government’s total expenditure and its total receipts excluding borrowing.

| Gross fiscal deficit = Total expenditure – (Revenue receipts + Non-debt creating capital receipts) |

1. Non-debt creating capital receipts are those receipts which are not borrowings and, therefore, do not give rise to debt. Examples are recovery of loans and the proceeds from the sale of PSUs.

2. From Table 5.1 we can see that non-debt creating capital receipts equals 10.0 percent of GDP, obtained by subtracting, borrowing and other liabilities from total capital receipts [1+4(a)+4(b)].

3. The fiscal deficit (GREEN BOXED), therefore turned out to be 3.5 percent of GDP.

4. The fiscal deficit will have to be financed through borrowing. Thus, it indicates the total borrowing requirements of the government from all sources.

5, Fiscal Deficit can also be defined from the financing side as

| Gross fiscal deficit = Net borrowing at home + Borrowing from RBI + Borrowing from abroad |

6. Net borrowing at home includes that directly borrowed from the public through debt instruments (for example, the various small savings schemes) and indirectly from commercial banks through Statutory Liquidity Ratio (SLR).

7. The gross fiscal deficit is a key variable in judging the financial health of the public sector and the stability of the economy.

8. From the way gross fiscal deficit is measured as given above, it can be seen that revenue deficit is a part of fiscal deficit (Fiscal Deficit = Revenue Deficit + Capital Expenditure – non-debt creating capital receipts).

9. A large share of revenue deficit in fiscal deficit indicates that a large part of borrowing is being used to meet its consumption expenditure needs rather than investment.

Primary Deficit

1. We must note that the borrowing requirement of the government includes interest obligations on accumulated debt.

2. The goal of measuring primary deficit is to focus on present fiscal imbalances.

3. To obtain an estimate of borrowing on account of current expenditures exceeding revenues, we need to calculate what has been called the primary deficit.

4. It is simply the fiscal deficit minus the interest payments.

| Gross primary deficit = Gross fiscal deficit – Net interest liabilities |