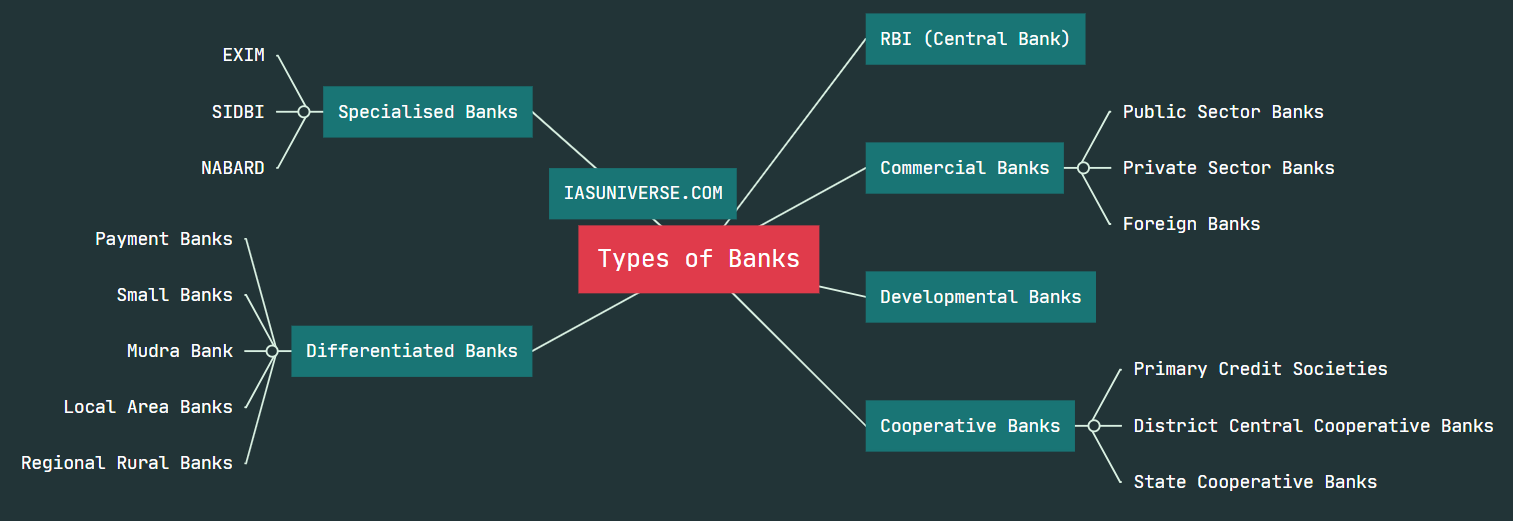

1.Differentiated banks are banking institutions licensed by the RBI to provide specific banking services and products.

2. Main aim for giving licenses to these banks is to promote financial inclusion and payments.

3. Differentiated banks licensing was launched in 2015.

4. They are niche banks that focus and serve the needs of a certain demographic segment of the population.

5. They also provide provision of small saving schemes to inculcate a saving culture.

Mudra Bank

1. MUDRA or Micro Units Development and Refinance Agency Ltd is a development and finance agency formed by the government of India.

2. Its aim is to provide refinancing and development functions to funding to the Non-Corporate Small Business Sector (NCSB) units, also called micro-unit enterprises. This is done through various financial institutions like Banks, NBFCs and MFIs.

3. MUDRA was launched with an aim to help micro-unit enterprises (around 50 crore people), as their growth performances influence the growth of the country.

Offerings by MUDRA

- The main function of MUDRA to provide finance to “Last Mile Financiers” such as Non-Banking Finance Companies, Trusts, Co-operative Societies, Small Banks, Scheduled Commercial Banks, Regional Rural Banks and Section 8 Companies which gives loans to small and micro-entities involved in manufacturing, trading, and services activities.

- Since small business owners and micro-unit enterprises are often cut off from the formal banking system (primarily because of limited branch presence) MUDRA Bank partners with local coordinators to provide finance to “Last Mile Financiers” of small/micro businesses.

- MUDRA targets young, educated or skilled workers and entrepreneurs including women entrepreneurs.

MUDRA and Pradhan Mantri MUDRA Yojana (PMMY)

MUDRA nurtures small businesses through Pradhan Mantri MUDRA Yojana (PMMY), which is a scheme launched by the Government of India and implemented through MUDRA.

The scheme consists of three loan products denoting the stage of growth the micro-enterprise is in. This is categorized into three stages: Shishu, Kishor, and Tarun.

- Shishu: As the name suggests, this stage of the business is when it is still taking its baby steps. The loan cover in this stage is up to Rs 50,000. `

- Kishor: The entrepreneur is eligible for a loan ranging from Rs 50,000 to Rs 5 lakh.

- Tarun: The final category will provide loans for up to Rs 10 lakh.

As per regulations, at least 60% of the loan amount should be given for Shishu categories. The MUDRA is also supposed to extend several development functions to the microfinance sector.

Payment Bank

1. The goal of establishing payments banks is to increase financial inclusion by providing (1) modest savings accounts (2) payments/remittance services to migratory workers, low-income families, small enterprises, other unorganized sector entities, and other users.

2. Customers will not be able to borrow from them.

3. Payment banks would be forced to invest their money in government bonds and bank deposits.

4. Examples: India Post Payment Bank, Airtel Payment Bank etc.

Small Finance Bank

1. Small finance banks are financial institutions that provide financial services to the country’s underserved and unbanked areas.

2. They are registered as a public limited company under the Companies Act, 2013.

3. These banks, like other commercial banks, can engage in all basic banking activities, such as lending and accepting deposits.

4. Small finance banks will be established with the goal of increasing financial inclusion by (1) providing savings vehicles and (2) providing credit to small businesses, small and marginal farmers, micro and small industries, and other unorganised sector entities through high-tech, low-cost operations.

5. The NachiketMor committee on financial inclusion suggested SFBs.

6. Small Finance Banks can’t extend big loans.

7. They Cannot float subsidiaries or trade in high-tech products.

8. Examples: Ujjivan small finance bank, Equitas small finance bank etc.

Difference between Small Finance Bank and Payments Bank

| Difference | Small Finance Bank | Payments Bank |

| Promoter | Small Finance banks are promoted by individuals with at least 10 years of experience in finance, NBFCs, local area banks, etc. | Payments Banks can be promoted by prepaid card issuers, telecom companies, NBFCs, business correspondents, supermarket chains, corporates, realty sector co-ops & PSUs. |

| Promoter’s Share | 40% in the beginning Then, over the next 12 years, it can be gradually reduced to 26%. | 40% for the first five years from the date of business start-up. |

| Capital Required | Min Paid Up capital should be 100 Cr | Min Paid Up capital should be 100 Cr |

| Customer | Mainly caters to small scale industries and farmers | Provide remittance services for migratory labourers and similarly unorganized sectors. |

| Demand Deposit | Can accept demand deposits as savings deposits are accepted, with no set limit. | Can accept demand deposits like savings deposit only upto Rs. 2 lakh. |

| Time Deposit | Can accept Time Deposit such as Fixed Deposit and Recurring Deposit. | Can’t accept Time Deposit such as Fixed Deposit and Recurring Deposit. |

| Loan | Can offer small loans.Must ensure that loans and advances, not exceeding Rs. 25 lakh, must constitute at least 50% of its loan portfolio. | Cannot offer loans.Are allowed to distribute mutual funds, insurance policies and other similar non-risk simple financial products. |

| Credit Card | Can issue credit cards | Cannot issue credit cards |

| Branches | 25% of branches must be in rural areas for the first three years. | Must have 25% branches in rural areas. |

Regional Rural Banks

1. Regional Rural Banks were established under (Ordinance of 1975) and the RRB Act 1987 to provide sufficient banking and credit facilities for agriculture and other rural sectors.

2. Regional Rural Banks (RRB) are Indian Scheduled Commercial Banks ( Government Banks) operating at regional level in different states of India. They have been created with a view of serving primarily the rural areas of India with basic banking and financial services.

3. However, RRBs may have branches set up for urban operations and their area of operation may include urban areas too.

4. The area of operation of RRBs is limited to the area as notified by Government of India covering one or more districts in the State.

5. RRBs are at par with commercial banks as far as compliance requirements to CRR and SLR is concerned.

6. Each RRB is owned by three entities with their respective shares as follows:

a. Central Government → 50%

b. State government → 15%

c. Sponsor bank→ 35%

7. PSL target of RRBs is 75% of total outstanding advances (PSL norm is 40% for a commercial bank).

8. RBI and NABARD are two prime regulators of RRBs.

RRBs perform various functions in following heads:

1. Providing banking facilities to rural and semi –urban areas.

2. Carrying out government operations like disbursement of wages of MGNREGA workers, distribution of pension etc.

3. Providing Para-Banking facilities like locker facilities, debit and credit cards, mobile banking, internet banking, UPI etc.

Local Area Banks

1. The Local Area Bank scheme was introduced in 1996 to create institutions that would provide financial intermediation with a specialized local focus in rural and semi-urban areas.

2. Local Area Banks (LAB) are banks set up by the Government of India solely to enable the local institutions to pool and mobilize rural savings and ensure that these savings are made available for investment concerning needs.

3. There are only four Local Area Banks (LAB) in India, which exist in the form of Non-scheduled banks.

(They are Coastal Local Area Bank Ltd, Capital Local Area Bank Ltd, Krishna Bhima Samruddhi Local Area Bank Ltd and Subhadra Local Area Bank Ltd., Kolhapur.)

Features of Local Area Banks (LABs):

- LABs are registered under the Companies Act, 1956, as a public-limited entity.

- A LAB licensed under the BRA or Banking Regulation Act, 1949. It means the LAB will have to operate per the Banking Regulation Act, 1949.

- A LAB is subjected to accounting policies, prudential norms, and other policies as laid by the Reserve Bank of India.

- A LAB is currently the only type of non-scheduled bank in India.

- Each LAB granted permission to open a branch in a single urban center in each district. The remaining branches are open in rural and semi-urban centers.

- Local Area Bank is set up as a private limited entity under the private sector to respond to the local’s credit and other financial needs and requirements, and that too in a competitive form.

- The banking activities of LAB are regulated and monitored by the RBI.

- LAB offers loans to locals for agricultural and other similar activities.

- A corporate house sets up LAB, individual, trust, society, etc., with a paid-up capital of at least INR 5 Crores.

- Usually, LABs are set in a district town. These are required to operate within their predetermined area, which in normal cases includes a maximum of 3 contiguous district towns.

- In a Local Area Bank system, the promoters can be firms, societies, or individuals.