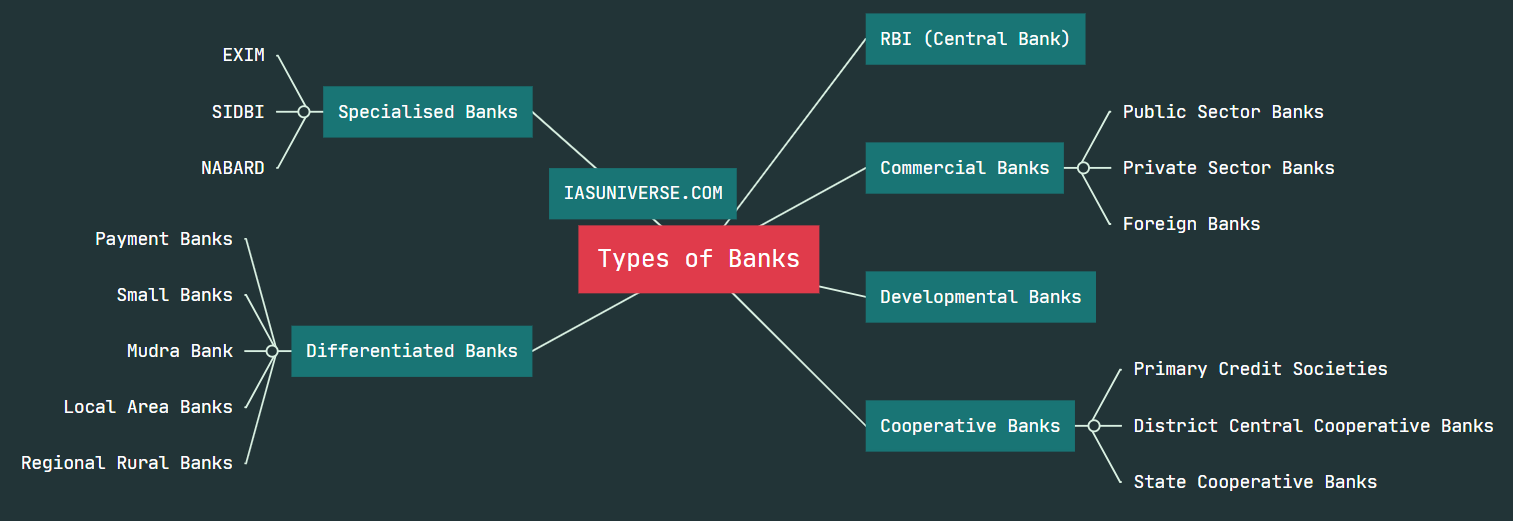

There are some banks, which cater to the requirements and provide overall support for setting up business in specific areas of activity.

Examples are: EXIM bank, SIDBI and NABARD.

EXIM bank

1. In September 1981, the Government of India passed the Export-Import Bank of India Act of 1981. Under this act, EXIM bank was set up to improve export credit.

2. The government of India wholly owns the EXIM bank, and the RBI regulates it.

3. The headquarters of EXIM bank is in Mumbai, Maharashtra.

4. EXIM bank aims to finance, facilitate and promote foreign trade in India.

Functions:

- Finances import and export of goods and services from India and countries other than India.

- Provides refinancing services to banks and other financial institutes for their financing of foreign trade.

- EXIM bank will also provide financial assistance to businesses joining a joint venture in a foreign country.

- The bank also provides technical and other assistance to importers and exporters. The EXIM bank will provide guidance and assistance in administrative matters as well.

- Undertakes functions of a merchant bank for the importer or exporter in transactions of foreign trade.

- Will also underwrite shares/debentures/stocks/bonds of companies engaged in foreign trade.

- It finances the import or export of machines and machinery on lease or hire purchase basis as well.

- Will offer short-term loans or lines of credit to foreign banks and governments.

- EXIM bank can also provide business advisory services and expert knowledge to Indian exporters in respect of multi-funded projects in foreign countries

SIDBI

1. SIDBI or the Small Industries and Development Bank of India was established under the special Act of the Parliament 1988 and became operative in the year 1990.

2. It is a wholly-owned subsidiary of IDBI (Industrial Development Bank of India).

3. SIDBI is the Primary Financial Institution for promoting, developing and financing MSME (Micro, Small and Medium Enterprise) sector.

4. SIDBI also promotes cleaner production and energy efficiency.

5. SIDBI was made responsible for administering the Small Industries Development Fund and National Equity Fund that were administered by IDBI before.

Financing facilities offered by SIDBI

1. Direct lending/finance: aims to fill the existing credit gaps in the MSME sector and is undertaken through demonstrative and innovative lending products

2. Indirect lending/finance: is undertaken through Banks, SFBs, NBFCs, MFIs and New Age Fintechs.

3. Micro finance: offers microfinance to small businessmen and entrepreneurs for establishing their business. Also, MUDRA is a subsidiary of SIDBI.

Functions of SIDBI

- Small Industries Development Bank of India refinances loans that are extended by the PLIs(priority sector lendings) to the small-scale industrial units and also offers resources assistance to them.

- It discounts and rediscounts bills.

- It also helps in expanding marketing channels for the products of SSI (Small Scale Industries) sector both in the domestic as well as international markets.

- It offers services like factoring, leasing etc. to the industrial concerns in the small-scale sector.

- It promotes employment-oriented industries particularly in semi-urban areas for creating employment opportunities and thus checking the relocation of people to the urban areas.

- It also initiates steps for modernisation and technological up-gradation of current units.

- It also enables the timely flow of credit for working capital as well as term loans to Small Scale Industries in cooperation with commercial banks.

- It also co-promotes state-level venture funds

What is MUDRA bank?

1. MUDRA or Micro Units Development and Refinance Agency Ltd is a development and finance agency formed by the government of India.

2. Its aim is to provide refinancing and development functions to funding to the Non-Corporate Small Business Sector (NCSB) units, also called micro-unit enterprises. This is done through various financial institutions like Banks, NBFCs and MFIs.

3. MUDRA was launched with an aim to help micro-unit enterprises (around 50 crore people), as their growth performances influence the growth of the country.

Offerings by MUDRA

- The main function of MUDRA to provide finance to “Last Mile Financiers” such as Non-Banking Finance Companies, Trusts, Co-operative Societies, Small Banks, Scheduled Commercial Banks, Regional Rural Banks and Section 8 Companies which gives loans to small and micro-entities involved in manufacturing, trading, and services activities.

- Since small business owners and micro-unit enterprises are often cut off from the formal banking system (primarily because of limited branch presence) MUDRA Bank partners with local coordinators to provide finance to “Last Mile Financiers” of small/micro businesses.

- MUDRA targets young, educated or skilled workers and entrepreneurs including women entrepreneurs.

MUDRA and Pradhan Mantri MUDRA Yojana (PMMY)

MUDRA nurtures small businesses through Pradhan Mantri MUDRA Yojana (PMMY), which is a scheme launched by the Government of India and implemented through MUDRA.

The scheme consists of three loan products denoting the stage of growth the micro-enterprise is in. This is categorized into three stages: Shishu, Kishor, and Tarun.

- Shishu: As the name suggests, this stage of the business is when it is still taking its baby steps. The loan cover in this stage is up to Rs 50,000. `

- Kishor: The entrepreneur is eligible for a loan ranging from Rs 50,000 to Rs 5 lakh.

- Tarun: The final category will provide loans for up to Rs 10 lakh

As per regulations, at least 60% of the loan amount should be given for Shishu categories. The MUDRA is also supposed to extend several development functions to the microfinance sector.

What is the difference between SIDBI bank and MUDRA bank?

| SIDBI | MUDRA |

| SIDBI (Small Industries and Development Bank of India) was established with a mission to facilitate and strengthen credit flow to micro, small and medium enterprises and became operative in the year 1990. | MUDRA (Micro Units Development and Refinance Agency Ltd) is a development and finance agency established by the Government of India and was launched on the 8th of April 2015. |

| SIDBI is a wholly-owned subsidiary of IDBI. | MUDRA is a subsidiary of SIDBI. |

| SIDBI offers a refinancing scheme to raise the position of Primary Lending Institutions as a dedicated lender in order to enable the flow of credit to the MSME sector. | MUDRA helps provide refinancing to the Non-Corporate Small Business Sector (NCSB). This is done through various financial institutions like Banks, NBFCs and MFIs. |

| SIDBI offers direct finance, indirect finance, and microfinance to its customers. | MUDRA nurtures small businesses through Pradhan Mantri MUDRA Yojana (PMMY), which consists of three loan products: Shishu, Kishor, and Tarun. |

| SIDBI helps MSMEs in acquiring the funds they require to grow, market, develop and commercialize their products. | MUDRA nurtures small businesses through Pradhan Mantri MUDRA Yojana (PMMY), a scheme launched by the Government of India and implemented through MUDRA. |

NABARD (National Bank for Agriculture and Rural Development)

The government of India established NABARD in 1982, under the outlines of the National Bank for Agriculture and Rural Development Act 1981.

NABARD is the main and specific bank of the country for agriculture and rural development.

Role of NABARD

- It coordinates the rural credit financing activities of all sorts of institutions engaged in developmental work at the field level while maintaining liaison with Government of India, and State Governments, and also RBI and other national level institutions that are concerned with policy formulation.

- It prepares rural credit plans, annually, for all districts in the country.

- It also promotes research in rural banking, and the field of agriculture and rural development.

- It is making efforts to establish linkages between Self-help Group(SHG) that are organized by voluntary agencies for poor and needy in rural areas and other official credit agencies.

- It refinances to the complete extent for those projects that are taken under the ‘National Watershed Development Programme‘ and the ‘National Mission of Wasteland Development‘.

- It also supports Vikas volunteer Vahini programs which offer credit and development activities to poor farmers.

- It also inspects and supervises the cooperative banks and RRBs to periodically ensure the development of rural financing and farmers’ welfare.

- NABARAD also recommends licensing for RRBs and Cooperative banks to RBI.

- It provides refinance for IRDP (Integrated Rural Development Programme) accounts in order to give the highest share for the support for poverty alleviation programs run by IRDP.

- Along with all the above roles, the National Bank for Agriculture and Rural Development also keeps the portfolio of the Natural Resource Management Programmes.

- Rural Infrastructure Development Fund (RIDF) is maintained by the NABARD. The RIDF was set up by the government during 1995-1996 for financing ongoing rural infrastructure projects. Banks which are not able to meet their targets of PSL (Priority Sector Lending) are required to keep the shortfall in RIDF.